The solar and storage market has undergone multiple seismic shifts throughout 2025, from the introduction of IEEPA tariffs to new AD/CVD and Section 232 cases. While these will continue to play a vital role in product pricing and supply chain developments, the looming foreign entity of concern (FEOC) restrictions and changes to solar tax credit eligibility and safe harbor requirements are the topics top of mind for most. What is the market reality today for solar and energy storage developers, IPPs, and EPC, and how must strategies shift to accommodate?

What’s changed?

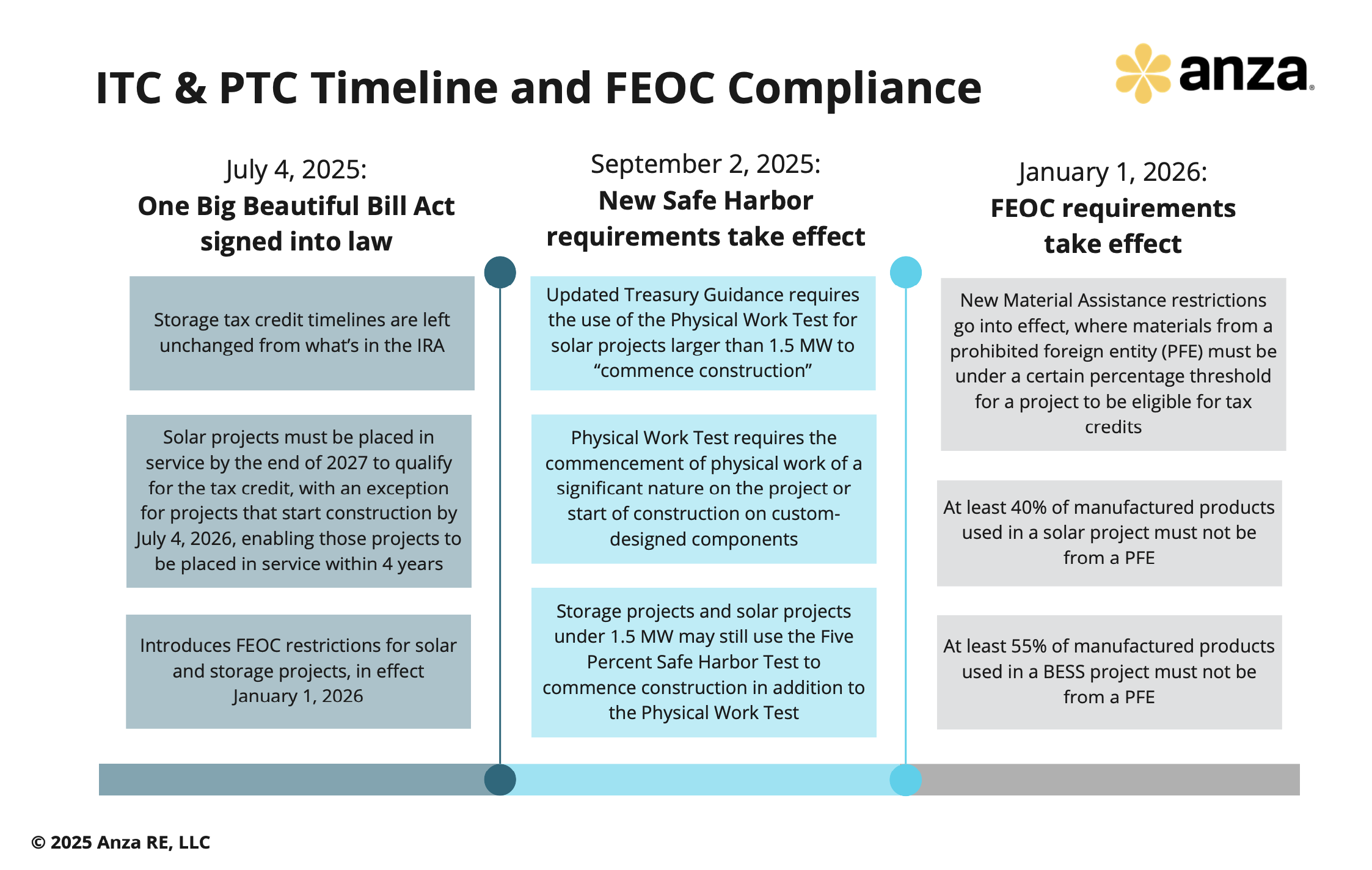

September 2, 2025, has come and gone, and with it, the 5% safe harbor test to commence construction on solar projects larger than 1.5 MW. Additionally, new FEOC restrictions are right around the corner, limiting tax credit eligibility for both solar and energy storage projects receiving material assistance from a prohibited foreign entity. As a recap, here’s what changed in Q3 2025 and what’s coming in 2026.

July 4, 2025: One Big Beautiful Bill Act signed into law

- Storage tax credit timelines are left unchanged from what’s in the IRA

- Solar projects must be placed in service by the end of 2027 to qualify for the tax credit, with an exception for projects that start construction by July 4, 2026, enabling those projects to be placed in service within 4 years. This is why many companies have already safe harbored projects via purchasing transformers or solar modules.

- Introduces FEOC restrictions for solar and storage projects, in effect January 1, 2026

September 2, 2025: New Safe Harbor requirements take effect

- Updated Treasury Guidance requires the use of the Physical Work Test for solar projects larger than 1.5 MW to “commence construction”

- The Physical Work Test requires the commencement of physical work of a significant nature on the project or the start of construction on custom-designed components (such as a transformer)

- Storage projects and solar projects under 1.5 MW may still use the Five Percent Safe Harbor Test to commence construction, in which 5% of the depreciable project basis is paid, in addition to the Physical Work Test

January 1, 2026: FEOC requirements take effect

- New Material Assistance restrictions go into effect, where materials from a prohibited foreign entity (PFE) must be under a certain percentage threshold (which increases annually) for a project to be eligible for tax credits

- At least 40% of manufactured products used in a solar project must not be from a PFE

- At least 55% of manufactured products used in a BESS project must not be from a PFE

What should my strategy be now?

Are you unsure about when FEOC applies or how it will impact your projects? Do you need help determining if a product and supplier are FEOC compliant? Anza’s data and experts can provide you with the clarity you need, so you always know what options are available. We’ve already collected extensive FEOC data from energy storage and solar suppliers and continue doing so on an ongoing basis, tracking a fluid supply chain landscape including the latest plans from suppliers exploring new cell capacity to reduce FEOC exposure.

Anza’s one-of-a-kind on-demand platform gives you supply chain transparency and the ability to filter products that will deliver the best returns while reducing risk. We recently added three new fields to our Energy Storage Pro data and analytics subscription, enabling users to quickly assess which energy storage system suppliers may face FEOC restrictions. Easily view a BESS supplier’s ownership structure and evaluate effective control, including whether they have operations in China. To help you better navigate FEOC compliance risks, we also provide a FEOC Risk Rating, which objectively determines the risk that a supplier will be categorized as a foreign entity of concern in their current supply chain structure, state of ownership, and effective control, based on government criteria. This information is easily accessible to Anza platform users in just a few clicks for better project planning and risk mitigation.

Additionally, we offer greater insights into solar and BESS FEOC compliance through our Market Insights service. Our team provides you with tailored analysis, helping you understand supply chain risk specific to your projects, such as a deep dive into FEOC compliance of a few specific suppliers, and applies up-to-date market knowledge to your strategy. For example, we are tracking Chinese OEMs, capturing their stated plans to change supply chain, ownership, and control, along with timing, so you can stay ahead of the curve and know FEOC-compliant suppliers that may be available down the road.

Depending on your project timing and strategy for utilizing tax credits, our current recommendations are as follows:

Battery Energy Storage System Projects

- Storage projects that were safe harbored before January 1, 2026, do not need to comply with FEOC under current law to be eligible for tax credits. For the rest of 2025, safe harboring is currently the best option, and as mentioned above, storage projects can still use the Five Percent Safe Harbor Test in addition to the Physical Work Test to commence construction.

- Buyers should consider safe harboring through energy storage system equipment due to price premiums, availability, and tariffs, such as the Section 301 25% tariff on battery cells and natural graphite (effective starting in 2026) and China IEEPA tariffs (set to take effect in November 2025).

- Anza has access to multiple suppliers who can deliver ESS blocks before the end of 2025. Our team is available to help buyers contract or get an LOI before the end of September to minimize the risk of shipment delays ahead of the FEOC cutoff.

- If you plan to purchase in 2026 and do not safe harbor by December 31, 2025, the FEOC-compliant supplier set may narrow. With the ITC available through 2032, it is critical to keep this in mind if your project economics rely on tax incentives. We expect more FEOC-compliant products to be available starting in mid-2026. Most suppliers will achieve compliance through non-China manufacturing and ownership changes, and we have started to receive early pricing indicators for FEOC-compliant options.

- If a project will not use the ITC, FEOC compliance does not apply. In some instances, especially for DG projects, FEOC equipment may still be the most cost-effective option, even without ITC benefits. Our team is available to help you determine what type of projects in your portfolio could pencil without the ITC and with or without FEOC compliant products so you can feel confident in your decision-making.

Solar Projects

- If you are planning on using the ITC for your solar project, there is still the option to safe harbor using the Physical Work Test through July 3, 2026, and place in service within four years.

- Several major suppliers have reached “sold out” status for 2025 delivery, and we are anticipating price increases from potential Section 232 tariffs on polysilicon and the India/Indonesia/Laos AD/CVD preliminary determinations in Q4 2025.

- For these reasons, our current recommendation is to lock in deals in the next 30-60 days before available inventory is gone and prices increase. We know from supporting over 2 GW of safe harbor procurements in 2025 and across 11 different vendors this summer what capacity is still available, what vendors have agreed to in contracts (like fixed price contracts), and what the best pricing looks like.

- Projects beginning construction starting January 1, 2026, will also need to comply with the new FEOC restrictions.

- If a project isn’t using the ITC, there’s no FEOC requirement. We expect that FEOC non-compliant suppliers will continue to sell into the U.S. market for the foreseeable future.

Whether FEOC applies to your project or not, or if you plan to use tax credits to increase margins, Anza is here to help. Schedule a demo today to find out more about the platform and services available to support your next project.